Banking & Finance

-> US Residential & Commercial Mortgage

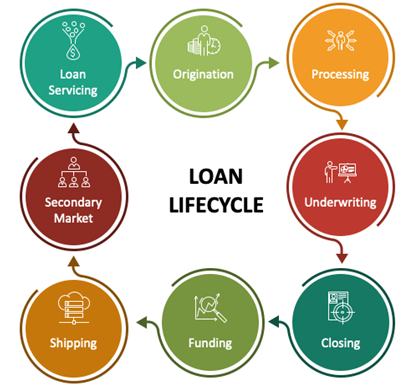

The mortgage life cycle starts when an individual decides to purchase a house and approaches a financial institution for the loan. It continues till the borrower repays the final payment to the mortgage provider.

Among the common money lending institutions that offer mortgage services, there are banks, credit societies, and mortgage companies. Mortgage is only offered to those individuals who can successfully prove their financial capability to repay the loan. The interest to be charged on the mortgage is then decided by the lender and depends on the various documents provided by the borrower endorsing his or her financial status. These documents usually include the income certificate, the credit score, and documents pertaining to any other loans that have been borrowed. The duration to pay back is chosen by the borrower which can also influence the rate of interest. The longer the duration, the lesser is the interest and vice versa.

Among the common money lending institutions that offer mortgage services, there are banks, credit societies, and mortgage companies. Mortgage is only offered to those individuals who can successfully prove their financial capability to repay the loan. The interest to be charged on the mortgage is then decided by the lender and depends on the various documents provided by the borrower endorsing his or her financial status. These documents usually include the income certificate, the credit score, and documents pertaining to any other loans that have been borrowed. The duration to pay back is chosen by the borrower which can also influence the rate of interest. The longer the duration, the lesser is the interest and vice versa.

US Residential & Commercial mortgage – End to End in mortgage process (Origination to Servicing). We provide servicing in Agency loans & Private lending/Hard money lending.

Agency loans are conventional fixed-rate, first mortgage loans secured by stabilized income-producing multifamily and manufactured housing communities that meet Fannie Mae and/or Freddie Mac underwriting guidelines.

Agency mortgage-backed securities (MBS) — Fannie Mae (FNMA), Freddie Mac (FHLMC) and Ginnie Mae (GNMA) — represent the second-largest segment of the US bond market after Treasuries and one of the most actively traded

Non-agency loans are backed by mortgage-backed securities issued by private financial institutions. These securities are also known as private-label securities

There are times you may help a buyer or seller without being their authorized representative. In this case you have a non-agency relationship, a situation where you have no binding or legal responsibility to the other party.

A private mortgage is a home loan financed through a private source of funds, rather than through a traditional mortgage lender. It can come in handy for people who struggle to get a mortgage the typical way.

As you evaluate the decision to borrow or lend through a private mortgage, keep the big picture in mind. Create a win-win solution where everybody gains financially without taking on too much risk.

The world is full of lenders, including big banks, local credit unions, and online lenders

Some borrowers might not be able to qualify for a loan from a traditional lender. Banks require a lot of documentation, and sometimes, a borrower's finances won't appear to be sound enough for the bank's preference. Even if you're more than able to repay the loan, mainstream lenders are required to verify that you can repay, and they have specific criteria to complete that verification. For example, self-employed people don't always have the W-2 forms and steady work history that lenders require, and young adults might not have good credit scores, because their credit histories are short.

Hard money lenders are generally private investors or companies that deal specifically in this type of lending. You won't find hard money loan options at your local bank. Hard money lenders aren't subject to the same regulations as traditional, conforming loan lenders

A hard money loan is a short-term, non-conforming loan for residential, commercial or investment properties, that doesn't come from traditional lenders, but rather people or private companies that accept property or an asset as collateral

A hard money lender is an investor who makes loans secured by real estate and usually lends on a short-term basis to real estate investors or developers. The investors/developers use the money to purchase and then renovate or develop properties.

-> Business Loans

A business loan is a loan specifically intended for business purposes. As with all loans, it involves the creation of a debt, which will be repaid with added interest.

The requirements to get a business loan

- Personal and business credit scores.

- A personal guarantee.

- Annual revenue.

- Years in business.

- Business industry and size.

- Business plan, financial statements, and loan proposal.

Term loans are one of the most common types of small business loans and are a lump sum of cash that you repay over a fixed term. The monthly payments will typically be fixed and include interest on top of the principal balance. You have the flexibility to use a term loan for a variety of needs, such as everyday expenses and equipment.

Small Business Administration (SBA) loans are enticing for business owners who want a low-cost government-backed loan. However, SBA loans are notorious for a long application process that can delay when you will receive the funding. It can take up to three months to get approved and receive the loan. If you don’t need money fast and want to benefit from lower interest rates and fees, SBA loans can be a good option.

Similar to a credit card, business lines of credit provide borrowers with a revolving credit limit that you can generally access through a checking account. You can spend up to the maximum credit limit, repay it, then withdraw more money. These options are great if you’re not sure of the exact amount of money you’ll need since you only incur interest charges on the amount you withdraw. That’s compared to a term loan that requires you to pay interest on the entire loan — whether you use part or all of it. Many business lines of credit are unsecured, which means you don’t need any collateral.

If you need to finance large equipment purchases, but don’t have the capital, an equipment loan is something to consider. These loans are designed to help you pay for expensive machinery, vehicles or equipment that retains value, such as computers or furniture. In most cases, the equipment you purchase will be used as collateral in case you can’t repay the loan.

Business owners who struggle to receive on-time payments may want to choose invoice factoring or invoice financing (aka accounts receivable financing). Through invoice factoring, you can sell unpaid invoices to a lender and receive a percentage of the invoice value upfront. With invoice financing, you can use unpaid invoices as collateral to get an advance on the amount you’re owed. The main difference between the two is that factoring gives the company buying your invoices control over collecting payments, while financing still requires you to collect payments so you can repay the amount borrowed.

Microloans are small loans that can provide you with $50,000 or less in funding. Since the loan amounts are relatively low, these loans can be a good option for new businesses or those that don’t need a lot of cash. Many microloans are offered through nonprofits or the government, like the SBA, though you may need to put up collateral (like business equipment, real estate or personal assets) to qualify for these loans.

Like traditional cash advances, merchant cash advances come at a high cost. This type of cash advance requires you to borrow against your future sales. In exchange for a lump sum of cash, you’ll repay it with either a portion of your daily credit card sales or through weekly transfers from your bank account. While you can often quickly obtain a merchant cash advance, the high interest rates make this type of loan a big risk. Unlike invoice financing/factoring, merchant cash advances use credit card sales as collateral, instead of unpaid invoices.

Becoming a franchisee can help you achieve your goal of business ownership quicker and easier than starting from the ground up, though you’ll still need capital. Franchise loans can provide you with the money to pay the upfront fee for opening a franchise, so you can get up and running. While you’re the one taking out the loan through a lender, some franchisors may offer funding to new franchisees.